Buying a home can be a huge undertaking. However, many of us might not have 20 percent down to purchase a home. An alternative? FHA loans can be a great option when purchasing a property, but there are a few things you should know first.

Home ownership is something many people strive for. We graduate college, save money for several years, and finally we have enough for a 20 percent down payment to purchase our first home.

This is a belief that many people have. We must have 20 percent down in order to purchase a home. That’s what we have been told. However, this couldn’t be farther from the truth. In fact, the Federal government wants more people to own real estate and they encourage you by providing low down payment options to purchase a home.

The Federal Housing Administration (FHA) is a mortgage issued by an FHA-approved lender and it is insured by the Federal Government through the Federal Housing Administration. These loans are typically designed for low-to-moderate-income borrowers, and they require minimum down payments, and modest credit scores as low as 500.

Currently, FHA requires only 3.5% down and you’ll need a 580 credit score to qualify. If your credit score falls between 500-579, you can still qualify for an FHA loan, however, you will be required to put at least 10% down. Your down payment for an FHA loan can come from your personal savings, a gift from family members, or a grant from down-payment assistance.

Understanding FHA Loans

One thing to note about FHA loans, is that the Federal Housing Administration doesn’t actually lend you the money, instead you get a loan from an FHA-approved lender, and the FHA guarantees the loans.

You must pay for this guarantee through mortgage insurance premiums. This is paid directly to the FHA every month and does not go away for the life of the loan. Lenders have less risk because if you stop paying for your loan and default, the Federal Housing Administration will pay your claim.

7 Things to Be Aware of Using an FHA Loan to Buy a Property

Types of FHA Loans

- Standard FHA Loans – This is what most people will use when getting an FHA loan. It requires 3.5% down and you can buy a 1-4 unit property.

- Home Equity Conversion Mortgage (HECM) – This is a reverse mortgage program that allows people over the age 62 to convert the equity in their home to cash, while retaining title to their home. You can withdraw funds on fixed monthly payments, through a line of credit, or both.

- FHA 203(k) Loan – This type of FHA loan is a construction loan that includes the cost of renovations/repairs into the loan. If you don’t have a lot of cash on hand, this will allow you to borrow for the home’s purchase price and renovations.

- FHA’s Energy Efficient Mortgage – This FHA loan program is similar to a FHA 203(k) loan, however, the renovations have to be geared towards lowering your utility bills. This includes new insulation, solar/wind energy systems, and energy efficient mechanicals.

- Section 245(a) Loan – This is an FHA loan program for people who expect their income to increase over time. Under a Section 245(a) program, mortgage payments start lower and gradually increase over time. The Growing Equity Mortgage also increases in monthly principal, resulting in shorter term loans.

Stable Income

It is important to know that FHA has no income or salary requirements to qualify for an FHA mortgage. You will, however, need to show stable income.

If you are an hourly employee, consistent pay stubs and tax returns will be very important. FHA lenders will want to see that you have worked at the same place for at least two years.

If you are a salaried employee you have a slight advantage to hourly employees. FHA lenders will look at offer letters for jobs and use that income to qualify you for a loan. Even if you have just landed a new job, they will still accept your offer letter as verified income.

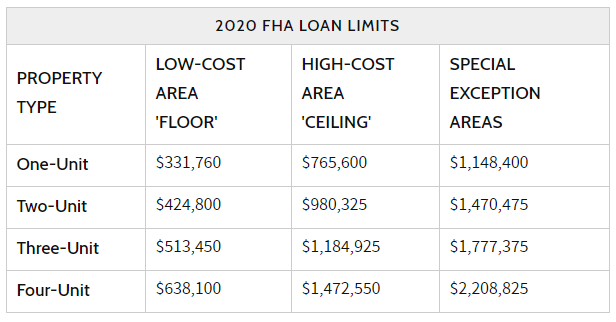

FHA Loan Limits

When deciding to use an FHA loan, you need to take into consideration the limits FHA has on how much you can borrow. These limits vary by the region that you live in. Low-cost areas have a lower limit, while high-cost areas have a higher limit. There are also special exception areas where construction costs are extremely high, resulting in even higher limits – these include – Alaska, Hawaii, Guam, and the U.S. Virgin Islands.

Everywhere else in the United States, has a set limit of 115% of the median home price as determined by the U.S. Department of Housing and Urban Development.

Below are the 2020 limits by area:

Should you use an FHA loan?

Just because an FHA loan is an option, it doesn’t mean you should necessarily use one. If you are an aspiring home owner who can afford 20% down with a traditional mortgage, that might be a better option. You will save money on closing costs and mortgage insurance premiums. You can also possibly receive better interest rates with a 20% down conventional mortgage over an FHA loan.

Moreover, the Federal Housing Administration states, an FHA loan “won’t accommodate those who are shopping on the higher end of the price spectrum—nor is it intended to. The FHA loan program was created to support ‘low- and moderate-income home buyers,’ particularly those with limited cash saved for a down payment.”

Consider your Debt-to-income Ratio

While your debt-to-income ratio is looked at with most mortgages you get, FHA loan officers won’t approve you if they don’t think you can make all of your obligated debt payments. This includes all your debts such as students loans, car payments, and credit card debt.

In general, your mortgage payment should be less than 31% of your income before taxes. FHA likes to see that your mortgage payments and your minimum payments towards other debts does not exceed 43%. However, in some cases, you can get approved if your debt obligations reach 50%.

Needs to be your primary residence

If you are using an FHA loan to purchase a property, it needs to be your primary residence. It cannot be a rental property or a vacation home.

You can, however, purchase a 2-4 unit property with an FHA loan, live in one unit, and rent out the others. This allows you to potentially live for free and it is called house hacking. Check out part 1 and part 2 of the 5 Step Process to House Hacking your Way to Financial Freedom. Another great aspect of purchasing a 2-4 unit property with an FHA loan is, they allow a portion of the rental income to help qualify you for the loan.

If you are interested in real estate investing, an FHA loan to house hack, a 2-4 unit property, is one of the best ways to get started.

Expect to pay more than 3.5% down

Yes, you only need to put 3.5% down on an FHA loan. The catch is, closing costs tend to be a bit higher than traditional mortgages. Closing costs include: mortgage insurance premium, lender fees, third party fees, and prepaid items. Mortgage insurance premiums are 1.75% of your total loan due at closing, making it one of the biggest differences between a conventional loan and FHA loan.

Be prepared to pay around 3-6% in closing costs when all is said and done. And this doesn’t include your 3.5% down payment. On a $250,000 mortgage, this is around $16,250 and $23,750 in total cash needed at closing. However, there are two potential workarounds.

Depending on how your current loan is structured, you might be able roll your closing costs into your total loan. This would allow you to finance the 3-6% in closing costs with your overall mortgage and you would only need to bring 3.5% for the down payment at closing. Talk with your lender to see if this is an option available to you.

The second workaround is, FHA allows the seller to pay up to 6% of the closing costs associated with the FHA loan for the borrower. Speak with your real estate agent to see if the seller is willing to do this.

How to qualify for an FHA Loan

When breaking everything down, these are the guidelines you must follow to be approved for an FHA loan:

- Credit score between 500 to 579 (Requires 10% down) or a credit score of 580+ to only put 3.5% down.

- Verifiable income for the last two years if you are hourly or commission based or proof of salary if you are a salaried employee

- Property must be used as a primary residence for at least one year

- Property is appraised by an FHA approved appraiser and it meets HUD property standards

- Your FHA mortgage payment should not exceed 31 percent of your gross monthly income.

- Your overall debt-to-income ratio should not exceed 43 percent of your gross monthly income. In some cases, lenders will allow up to 50 percent.

- If you have filed for bankruptcy in the past, you must wait 12 months to two years before you can apply

- You must wait three years to apply for an FHA loan if you have experienced a foreclosure. Lenders may make an exception to borrowers with certain circumstances.

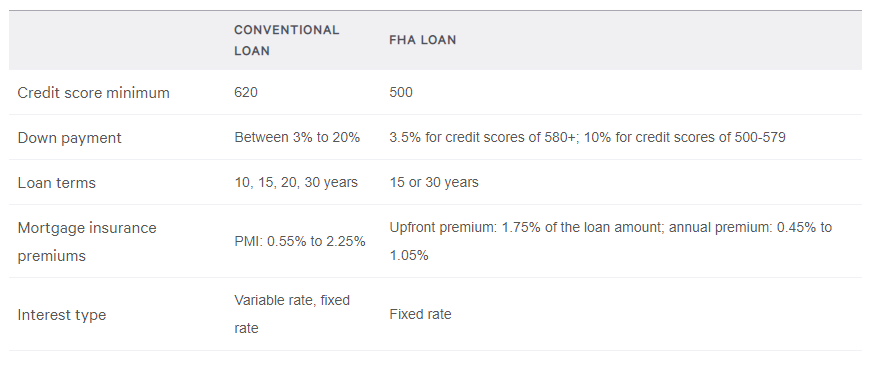

A quick glance: FHA loans vs Conventional loans

Conclusion:

Home ownership should be available to everyone. It is a part of the American dream. FHA loans make this a reality by helping thousands of people every single year who never thought it could be possible.

While an FHA loan isn’t right for everyone, it is a great option. Just be sure to educate yourself on the ins-and-outs of these loans and make sure it is the right fit for you.

Personal Experience with FHA Loans:

At this point, I want to share my own personal experience with FHA loans. After I graduated college, I knew I wanted to buy a duplex to live in one half and rent out the other. I didn’t have a lot of money saved up, so I had limited options.

I got a job that was salaried and I was able to qualify for an FHA loan by sending my lender my offer letter. Even though I did not have two years of work history, I was still able to qualify. I ended up purchasing a duplex with an FHA loan and lived completely for free.

Fast forward only six months, I moved to another state for a job andI kept my duplex with an FHA loan on it. I then rented out both units to earn extra income. However, I wanted to buy another duplex in the new state I was living in, just like before.

Again, I did not have much money saved up because I was paying down my student loans. After doing some research, I discovered I could possibly get another FHA loan; meaning I would have two FHA loans out at the same time. Only certain circumstances apply to allow this to happen and moving out of state for work was one of those reasons.

I ended up speaking with a great lender and I was approved for another FHA loan. I now own two duplexes, both with FHA loans on them. It took a lot of persistence, paperwork, and many hours to work through both FHA loans, but in the end it has allowed me to own two properties – making it well worth it.

Do you have personal experience with an FHA loan? If so, let’s hear about it and comment below!